SMM, December 27:

As the year-end approaches, zinc oxide production has recently shown a significant decline. Why is the market behaving this way? How will it perform in Q1? We analyze from multiple perspectives.

Firstly, orders in certain segments of zinc oxide have recently experienced a noticeable decline. Q4 is traditionally the peak season for automobile production and sales, with semi-steel tire production remaining robust, supporting related rubber-grade zinc oxide orders. However, with the arrival of winter, many ceramic factories began their holidays early in December, leading to a reduction in ceramic-grade zinc oxide orders, and some zinc oxide factories followed suit by halting production. Additionally, feed-grade zinc oxide orders in Q4 have shown a weaker-than-expected peak season performance. By the year-end, some large feed factories had already completed their stockpiling orders, while smaller factories showed limited recovery, resulting in a slight reduction in related zinc oxide orders recently.

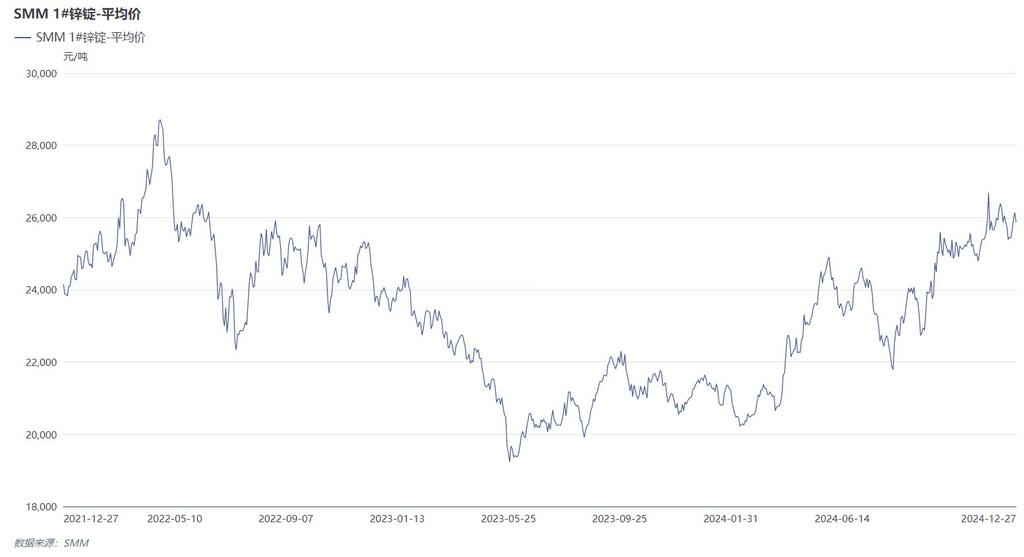

Secondly, zinc oxide enterprises have limited stockpiling at the year-end. According to SMM, as the year-end approaches, zinc prices continue to fluctuate at highs. Due to factors such as high raw material costs and poor orders, some enterprises have shown low willingness to stockpile overall. Although some electronic-grade zinc oxide enterprises have increased production to stockpile finished products, the overall boost to zinc oxide production remains limited.

In summary, affected by weakening orders, some factories have started their holidays early and halted production, leading to a significant decline in zinc oxide production recently. Entering January, some enterprises are concerned about a potential weakening of rubber-grade zinc oxide orders, while stockpiling orders in other segments are also largely completed. Coupled with the Chinese New Year holiday closures of zinc oxide manufacturers, overall zinc oxide production is likely to continue declining.

For SMM lead and zinc industry data packages, please contact: Penghui Tang, Manager

Phone: 15008461791